Finding Your Financial Power After 40: A New Zealand Woman's Guide to Mid-Life Wealth Confidence

Mid-life can be a turning point—not a setback.

For women over 40 in New Zealand, this decade often brings heightened earning power, accumulated wisdom, and a clearer sense of priorities. Yet many of us still feel uncertain about money. At Athena Wealth, we see this pattern shift when women gain clarity about their choices and understand the trade-offs that matter most to them.

Why Mid-Life Matters for Your Wealth

Between 40 and retirement, most Kiwi women navigate career peaks, caregiving responsibilities, relationship changes, and a shrinking investment horizon. The decisions you make now—about KiwiSaver, property, diversification, and risk—will echo for decades. This isn't about chasing the "perfect" strategy; it's about building confidence through informed choice.

Read our blog on 5 Tips to Thrive.

Key insights

Clarity Over Complexity

Mid-life wealth confidence starts with understanding your options, not memorising jargon.

Trade-Offs, Not Perfection

Every choice — property, shares, KiwiSaver — comes with different risks, liquidity, and returns.

Your Timeline Matters

The closer you are to retirement, the more important it is to balance growth with accessibility.

Two Paths, Different Outcomes: Property vs Diversified Investing

Many New Zealand women feel pressure to "get on the property ladder" as the gold-standard wealth builder. Property can deliver strong returns—but it's not the only option, and the numbers tell a nuanced story.

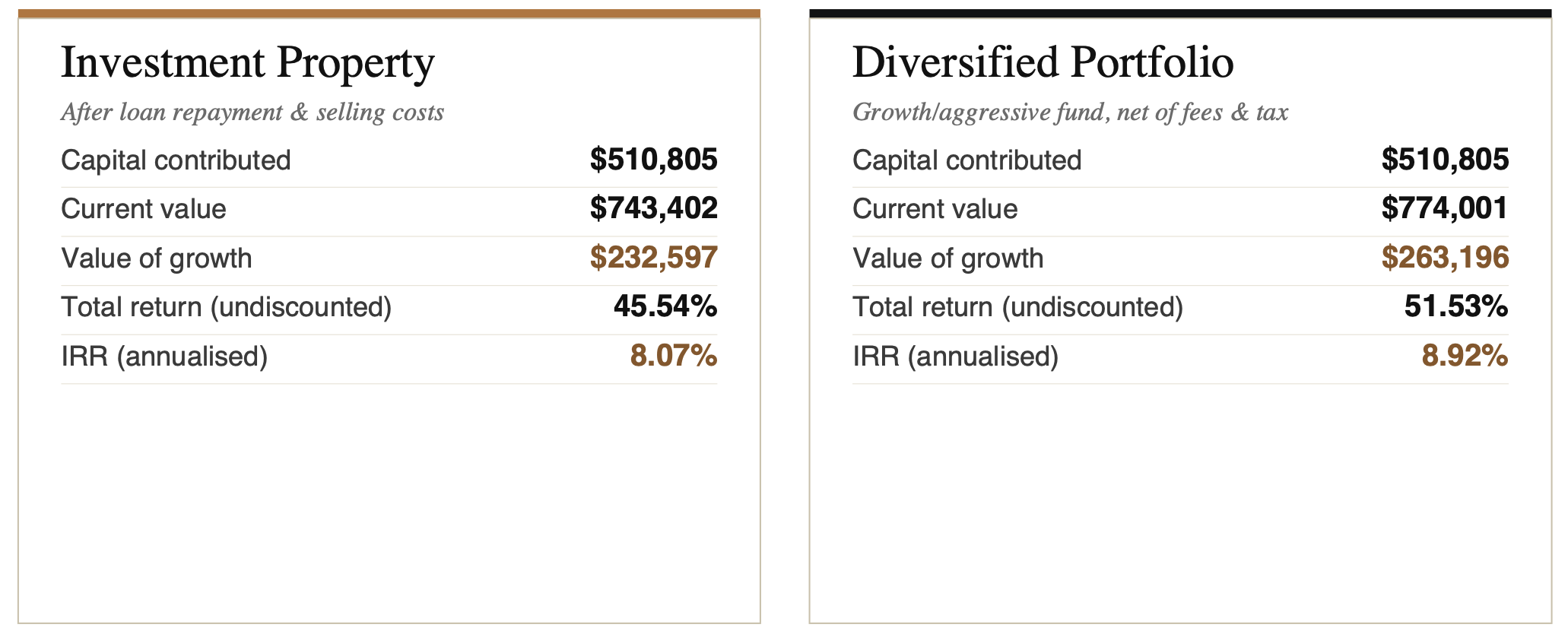

Consider this comparison: You have worked hard to pay off your home loan and increased the equity in your home. Using the equity you decide to buy a residential investment property.

A $1 million investment property (100% financed) requires approximately $510,805 in top-ups over 10 years to cover shortfalls. After loan repayment and selling costs, the internal rate of return (IRR) is 8.07% annually.

By contrast, investing the same capital progressively into a diversified aggressive portfolio yields an IRR of 8.92%—a 0.84 percentage point advantage. The diversified option also offers liquidity, lower concentration risk, and no tenancy headaches.

Result showing in the downloadable report from the Athena Investment Property Assessment Calculator.

This doesn't mean property is "wrong." It means understanding the full picture: capital intensity, cashflow demands, and opportunity cost. For women juggling caregiving or irregular income, liquidity and flexibility often matter more than raw returns.

The Long View: New Zealand Property Since 1990

House prices have grown significantly over the past 35 years. The RBNZ House Price Index that shows the Capital Growth, rose from a baseline of 100 in March 1990 to 615.5 by December 2025—a cumulative increase of 515.5%, or approximately 5.3% annually.

Performance overview

Average Annual Returns

Long-term performance across rolling time periods

Note Long-run averages of ~5%+ have moderated in the most recent 5-year window to 1.91% — a reminder that shorter horizons can deviate sharply from long-term trends.

Yet this growth hasn't been linear. Prices surged to a peak of 627.5 in 2021 before moderating. For women in their 40s and 50s today, this context is critical: property remains a wealth-builder, but timing, location, and leverage all matter.

A Diversified Portfolio: The Quiet Wealth Builder

While property dominates dinner-party conversations, Managed Funds in a Growth portfolio and KiwiSaver funds have quietly delivered consistent, compounding returns for New Zealanders. Over the 10 years to December 2025, category averages ranged from 4.2% (Conservative) to 9.5% (Aggressive) annually.

Growth and Aggressive funds—holding 72–94% in shares and property—delivered 8.2% and 9.5% respectively. For women with 15–25 years until retirement, these categories offer meaningful inflation protection and compound growth. Yet many of us remain in Conservative or Moderate funds due to inertia, not intention.

KiwiSaver performance

KiwiSaver Annualised Returns by Category

10-year vs. 5-year returns (% p.a.) to December 2025

Source Morningstar KiwiSaver Survey, December 2025 — category averages, after fees and before tax. The 5-year window has trailed the 10-year across every category, with the gap widening for lower-risk profiles.

The key insight? Risk tolerance should match your timeline, not your comfort zone. A 45-year-old with two decades to retirement can weather short-term volatility for long-term gain.

Three Steps to Mid-Life Wealth Confidence

1. Know your numbers.

Calculate your current KiwiSaver balance, projected retirement needs, and any gaps. Athena Wealth's property calculator (used in this analysis) can model trade-offs between property and portfolios. Link to the Investment Property Assessment Calculator

2. Align risk with reality.

If you're 40–55 with stable income, consider setting up a Managed Funds portfolio alongside your KiwiSaver in a Growth or Balanced fund. Review annually.

3. Diversify beyond property.

If you already own your home, adding shares, bonds, or managed funds can reduce concentration risk and improve liquidity. Your surplus income does not have to be added to KiwiSaver. Instead investing in a managed fund portfolio to suit your goals is a better option as it gives you liquidity.

Final Thought

Mid-life isn't about "catching up"—it's about claiming clarity.

Whether you choose property, an independent managed fund portfolio for investing alongside your KiwiSaver, the power lies in understanding what you're trading off and why. At Athena Wealth, we believe women thrive financially when they move from overwhelm to ownership of their choices.

Ready to feel more confident about your next financial chapter?

At Athena Wealth, we work with women across New Zealand who want clarity, not complexity. Whether you’re weighing up property versus investing, reviewing your KiwiSaver strategy, or simply wanting to understand what your current choices mean for the future, a conversation can bring valuable perspective.

If you’d like help turning information into a plan that reflects your life, values, and priorities, have a chat with Sumita.

Explore where you’re on track, where you may have options, and what confidence could look like for you.

Because financial confidence isn’t about doing more — it’s about understanding better.

Sources

Reserve Bank of New Zealand (RBNZ) – Housing M10 / House Price Index (HPI)

HPI indexed to March 1990 = 100

December 2025 HPI ≈ 615.5

Long‑term annualised growth ≈ 5.3% p.a.

Source data: RBNZ, CoreLogic, Statistics New Zealand.

Morningstar KiwiSaver Survey – December 2025

© Morningstar, Inc. Used for general educational comparison.

Supporting Context (Public NZ Sources)

4. Financial Services Council (FSC) – Insights and Trends: Women and Finance in New Zealand

Research highlighting financial confidence, barriers, and behaviours of Kiwi women.

5. Athena Wealth Blog – Midlife Money Makeover: 5 Tips for Women to Thrive Financially

Athena Wealth perspective on common mid‑life financial challenges and opportunities for women in New Zealand.

Important Disclaimer

This article is for general educational purposes only and does not constitute personalised financial advice. The investment property and portfolio scenarios presented are illustrative examples based on specific assumptions and may not reflect your individual circumstances. Past performance of KiwiSaver funds and property is not a reliable indicator of future results. Before making any investment decisions, please consult a qualified Financial Adviser who can assess your personal situation, goals, and risk tolerance.